Posted by Challenger 8/17/20

Some great statistics from a survey conducted in August 2020

Four months ago, sales pipelines abruptly dried up, leaving sales leaders deeply uncertain about the future. These days, we're seeing evidence of an uncertain, but emergent recovery; though a large number of our respondents’ report declines, more report the growth in opportunities, and reasons for optimism - and they're beginning to work these ideas into their Q4 plans.

Here is an in-depth look from a survey of sales organizations to get answers about the current state of affairs compared to April when the old proverbial s..t hit the fan.

Overall sentiment

The decline in sentiment is pretty consistent across individuals, their organizations, and the business environment generally (5% to 8%). Sales leaders continue to be a little more optimistic about their own fortunes and only slightly less optimistic about their organizations’, but only a minority are confident in the future business environment. It’s said, “a recession is when your neighbor loses their job, a depression is when you lose yours”. These numbers show we’re in recession, not depression, territory.

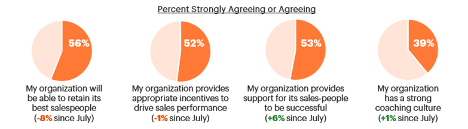

Sentiment with regards to sales management practices

We continue to see a decline in confidence that sales organizations will be able to retain their best people. 72% were confident of retaining their best in June, but this has now steadily fallen to 56%: a potential long-term problem that will likely make a return to growth more difficult in 2021

On the plus side, organizations have clearly made headway in their ability to support their salespeople. It appears investments in the various support resources we studied in July are starting to prove beneficial. You can find these details here, in July’s pulse survey.

Expectations for Q4 2020

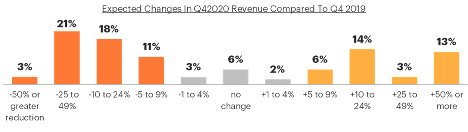

On average, respondents told us that they expect to deliver almost 1% less revenue in Q4 2020 than they did in the same quarter last year. Though a small overall reduction, the average hides considerable variation across firms. In our sample, we find that 36% expect to post good-to-great increases in revenue compared to 2019 (these are the lucky segments selling “essential” products). For a smaller percentage, 11%, life is steadier with no big difference in 2020 forecasted. The remainder of sales leaders (53%), however, expect to post sharply reduced revenues.

While our sample isn’t large enough to identify more definite trends, we did find respondents from the Health Care, Financial Services, High Tech, and Consumer Packaged Goods are forecasting solid growth. Respondents working for Transportation, Energy, Hospitality, Telecommunications , Business Services and Manufacturing firms, on the other hand, expect the largest declines in revenue. Overall, larger companies report doing better than smaller companies.

Business Priorities

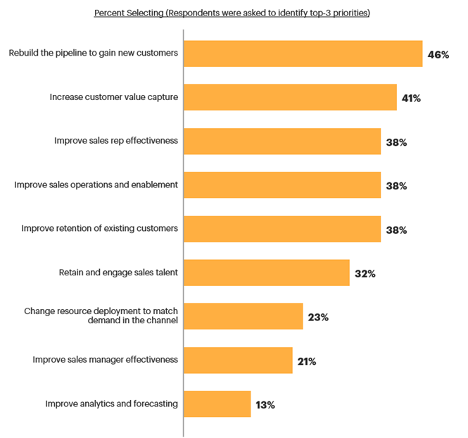

Lukewarm sentiment with regards to the economic future combined with a wide variation in revenue performance starts to explain sales leaders’ business priorities for 2021. At the top of the list (and the percentage goes up to 57% for more senior respondents) is a focus rebuilding the pipeline, followed by increasing customer value. Sales leaders indicate wanting to do that through a combination of improving sales rep effectiveness and better sales operations/enablement.

This continued focus on rebuilding the pipeline tells us sales organizations are still testing value propositions they started to build in April (66% told us that they were working on new value propositions at that time).

Shifts in the Pipeline

Four months ago, we observed many sales pipelines nearly grind to a halt. Customers were making only necessary purchases and re-evaluating all existing agreements. Now, a few months later, we are seeing evidence of an uncertain, but emergent recovery:

- Customers are more willing to have conversations (although 44% of respondents still report a decline)

- A larger number of opportunities have started to enter the pipeline although a majority still report a decline

- Deal sizes seem to be stabilizing, with fewer sales leaders reporting declines

- A real positive trend comes with conversion rates. Given significant market uncertainty in April, many sales leaders (63%) expected conversion rates to fall, but for many the opposite has happened. The overall reduction in opportunities has sifted out non-serious buyers and many companies have unexpectedly seen an increase in conversion rates. Those expecting a decrease has fallen as well by more than half.

- Another positive trend comes from cycle times. In April, the greatest number of sales leaders (41%) expected them to go up. But many experienced the opposite. Those customers still in the market have urgent needs and are willing to act decisively. Those expecting cycle times to increase has fallen by half.

- Sales leaders are clearly worried about future deal complexity, with a majority (51%) now expecting the role of finance to increase in the decision-making process. Greater involvement of Finance in purchasing seems here to stay.

- Similarly, we see no evidence that buying groups have shrunk in size: Instead we have good reason to believe the companies are now inviting more stakeholders to participate in due diligence than before. Due diligence processes tend to be sticky and so we believe that selling has only become more complicated.

|

April |

August |

April |

August |

April |

August |

|

|

A decline (-5% or less) |

A decline (-5% or less) |

More or less the same |

More or less the same |

An increase (+5% or more) |

An increase (+5% or more) |

|

|

Customer willingness to have conversations |

50% |

44% |

28% |

32% |

11% |

24% |

|

Number of active opportunities entering the pipeline |

77% |

57% |

19% |

17% |

5% |

25% |

|

Deal Size |

43% |

39% |

51% |

37% |

6% |

23% |

|

Conversion Rate |

63% |

30% |

30% |

35% |

8% |

35% |

|

Length of Sales Cycle |

37% |

43% |

22% |

37% |

41% |

20% |

|

Involvement of Finance in buying decisions |

9% |

8% |

55% |

41% |

36% |

51% |

|

Number of buyers involved |

9% |

7% |

68% |

45% |

22% |

48% |

Summary

Overall, sales leaders are still wary about the future state of the economy. And they have good reason: While some respondents project solid growth in Q4, a larger number expect substantial contraction. Similarly, while the sales pipeline has now somewhat normalized, a majority still report a significant decline in the number of opportunities entering the pipeline. This, for most, is the primary problem to solve. As a consequence, business leaders are actively looking for sources of new business, they are working to do a better job of capturing value from existing customers and they are helping their sales people be as effective as possible selling into a far more complex environment.

Bottom line message: Don’t wait to improve the caliber of your sales team!

We can help you measure what the strengths and limitations of your existing team are and then tell you definitively what you must do to thrive AND

we can provide you with the top sales candidate assessment on the market so that you can select top performers on purpose. No time for mistakes now!

Please call for further information. 800 700 6507